Construction Mortgages

Progress Advance Product Overview

Building a custom home in Nova Scotia requires a specialized financing approach. Unlike a traditional mortgage where funds are released all at once, a Construction Mortgage (or Progress Advance) provides funding in stages as your home reaches specific milestones of completion.

1. THE PROGRESS ADVANCE PROCESS

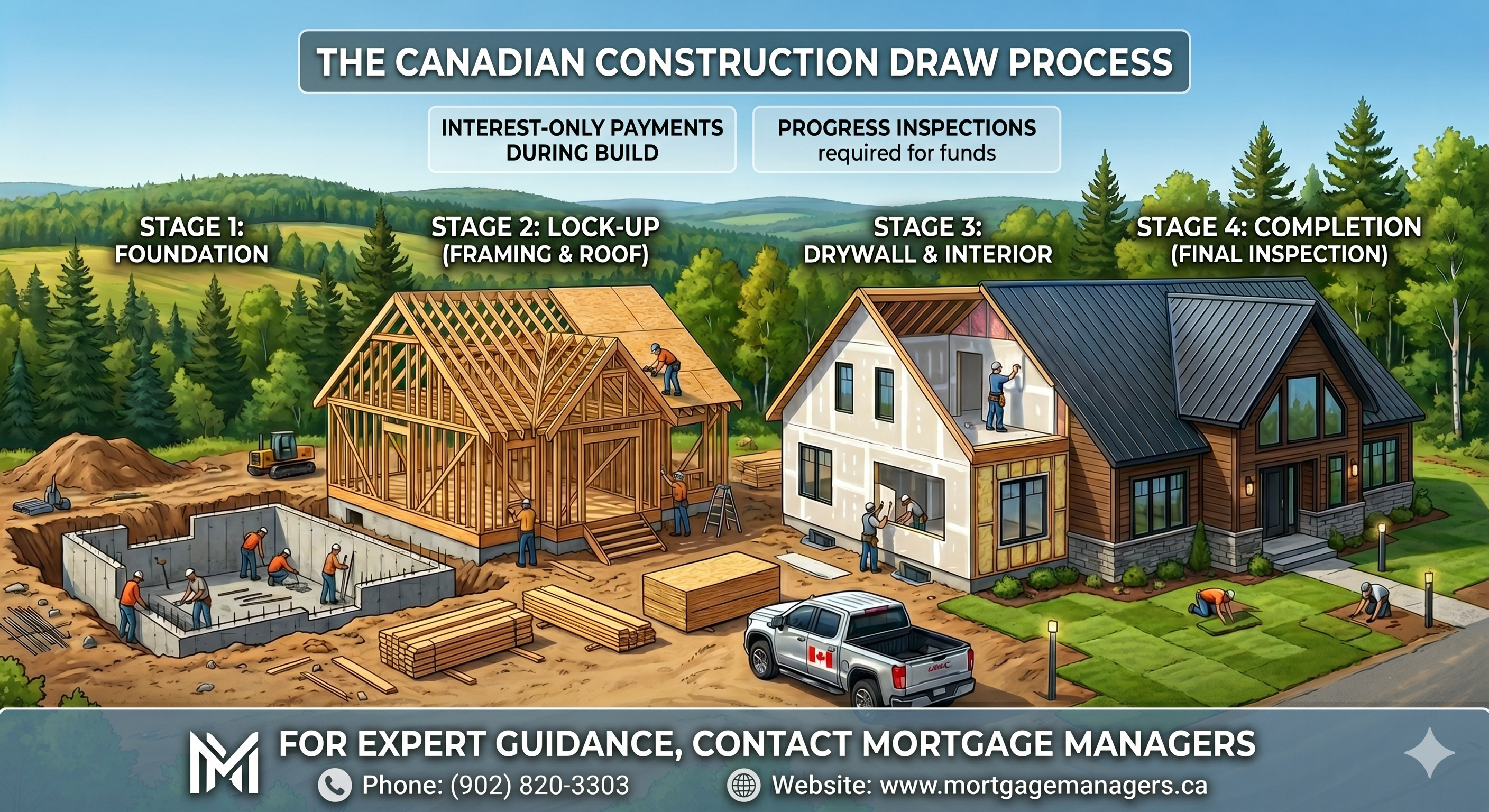

Funds are typically released in four main stages, verified by an appraiser’s inspection at each interval.

Stage Milestone Details:

2. LAND ADVANCE OPTIONS

If you are starting from the ground up, we can assist with the initial land purchase or leverage the equity in land you already own.

- Serviced Land: Up to 75% LTV (Loan-to-Value).

- Raw Land: Up to 50% LTV.

- Integration: The land advance is typically wrapped into the first construction draw, allowing for a seamless transition into the building phase.

3. QUALIFYING CRITERIA

To ensure a smooth approval process, the following standards generally apply:

- Credit Score: Minimum beacon score of 650 (no recent bankruptcies).

- Debt Ratios: Maximum GDS of 39% / TDS of 44%.

- Cost Overrun: Borrowers must demonstrate a 15% cost overrun contingency (liquid assets or line of credit).

- Down Payment: Minimum 5% for properties up to $500,000; 10% on the portion above $500,000.

4. REQUIRED DOCUMENTATION

- Signed building contract or detailed construction cost estimates.

- House plans and specifications.

- Building permits and New Home Warranty certificate (if applicable).

- Verification of income and down payment.

WHY CHOOSE MORTGAGE MANAGERS?

Navigating the complexities of draws, inspections, and holdbacks requires expert guidance. As local mortgage professionals serving Nova Scotia, we manage the details so you can focus on your build.

- Local Expertise: Deep knowledge of the Halifax and Hammonds Plains real estate markets.

- Strategic Planning: We coordinate with lenders and appraisers to ensure your funds are available when your contractors need them.

- Flexible Options: Access to both bank and alternative construction products to fit your unique financial profile.