Top 5 Common Mistakes First Time Home Buyers Make, and How To Avoid Them

April 06 2026

Buying your first home is one of the most exhilarating milestones you’ll ever reach. But in the 2026 real estate market—where inventory is shifting and lending criteria are stricter than ever—it’s also a high-stakes financial maneuver.

Even a small misstep can cost you thousands or, worse, result in losing your dream home at the finish line. To help you navigate the process with confidence, here are the top 5 common mistakes first-time home buyers are making right now and how you can avoid them.

1. Confusing "Pre-Qualification" with "Pre-Approval"

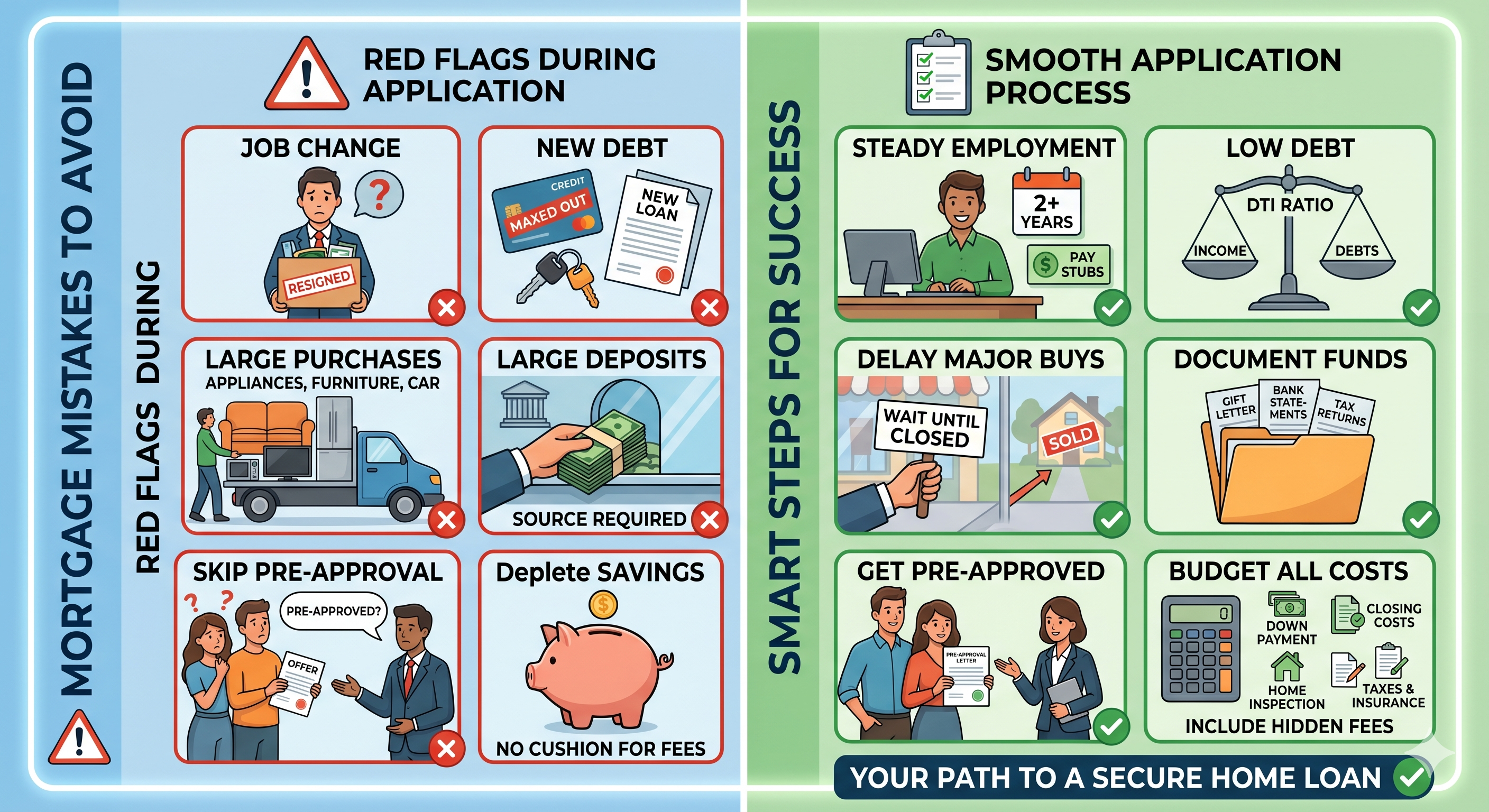

In a competitive market, a pre-qualification letter isn’t worth much more than the paper it’s printed on. A pre-qualification is usually just a "soft" estimate based on what you tell a lender. A Full Pre-Approval involves a deep dive into your tax returns, pay stubs, and credit report.

- The Risk: You fall in love with a house, make an offer, and then discover the bank won't actually lend you the amount you need.

- The Fix: Get a verified pre-approval before you even look at a single listing. This gives you a clear "buying power" number and makes your offer much more attractive to sellers.

2. Underestimating the "Hidden" Costs of Ownership

Many first-time buyers focus solely on the monthly mortgage payment. However, the purchase price is just the tip of the iceberg. You also need to budget for:

Closing Costs: Legal fees, land transfer taxes, and title insurance (typically 2–5% of the purchase price).

Maintenance Reserves: A leaky roof or a broken HVAC doesn't have a landlord to fix it anymore.

Ongoing Expenses: Property taxes, home insurance, and potential HOA/Condo fees.

- The Risk: Becoming "house poor"—having a beautiful home but no money left for groceries, travel, or emergencies.

- The Fix: Use a total cost calculator that includes taxes and maintenance. Aim for a mortgage payment that leaves you with a comfortable monthly cushion.

3. Making Major Financial Changes Before Closing

Once you are pre-approved, your financial profile is "frozen" in the eyes of the lender. A common mistake is going on a celebratory shopping spree for new furniture, financing a car, or even switching jobs right before the deal closes.

- The Risk: These actions change your Debt-to-Income (DTI) ratio. Lenders often do a final credit check just days before closing; if your debt has increased, they can—and will—pull the funding.

- The Fix: Don’t open new credit cards, take out loans, or make large, undocumented deposits until you have the keys in your hand.

4. Letting "Love" Blind Your Logic

It’s easy to get swept away by a stunning kitchen or a perfect backyard. When emotions drive the purchase, buyers tend to overlook major structural red flags or overpay significantly just to "win" the house.

- The Risk: You end up with a "money pit" or a home that doesn't actually meet your long-term needs (like proximity to work or school).

- The Fix: Create a "Must-Have vs. Nice-to-Have" checklist. If a house doesn't meet the "Must-Haves," walk away—no matter how pretty the staging is.

5. Waiving the Home Inspection to "Be Competitive"

In tight markets, some buyers waive the inspection to make their offer more appealing to the seller. In 2026, this is one of the most dangerous gambles you can make.

- The Risk: You could inherit foundation issues, outdated wiring, or mold problems that cost tens of thousands of dollars to repair.

- The Fix: Never skip the inspection. If you’re in a bidding war, try shortening the inspection window to 48 hours instead of waiving it entirely. Knowledge is your best negotiating tool.

Ready to Start Your Journey?

Navigating the road to homeownership doesn't have to be overwhelming. The right team can help you avoid these pitfalls and ensure your first home is a sound investment for your future.

Contact Mortgage Managers for more info and let us help you secure a mortgage that fits your life and your goals.