July 20 2026

When you apply for a mortgage in Canada, your lender looks closely at your income, debt load, and credit history. If your numbers fall a bit short of their guidelines—or if you need help passing the mortgage stress test—the lender may ask you to bring...

Read Post

May 31 2026

Saving for a down payment while dealing with today’s rental market can feel like trying to run a marathon in quicksand. It is no secret that rising costs have made the traditional path to homeownership incredibly frustrating for first-time buyers right here in Nova Scotia.

Read Post

May 21 2026

The big banks rarely explain this upfront, probably because it is such a confusing calculation. Try asking Google or Claude.ai and you will get a wide range of explanations, some of them incorrect. Or, try to find infomation about Prepayment Penalties on the bank's own...

Read Post

May 18 2026

For most Nova Scotian homeowners, your property is more than just a place to live—it is a wealth-building asset. Over time, as you pay down your mortgage and property values change, you build up equity. But that equity does you little good if it is just sitting...

Read Post

May 14 2026

Applying for a mortgage can feel like a mountain of paperwork, but it doesn’t have to be overwhelming. The difference between a smooth, stress-free approval and a week of back-and-forth emails often comes down to one thing: preparation.

Lenders need a clear "financial story" of...

Read Post

May 12 2026

Buying a home in Nova Scotia is one of the most significant financial milestones in life, but if your credit score isn’t where you want it to be, the process can feel overwhelming. The good news is that "bad credit" doesn't have to be a permanent ...

Read Post

April 30 2026

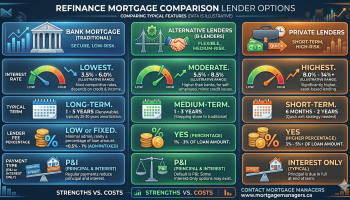

After 22 years of being mortgage brokers here in Hammonds Plains, Nova Scotia, we have developed relations hips with a wide range of top quality mortgage lenders, from Main Street banks to very flexible Private Lenders, each having their own niche/specialty. For simplicity, let's ...

Read Post

April 27 2026

Building your dream home in Nova Scotia from the ground up is an exhilarating journey, but from a financing perspective, it’s a bit of a different beast than buying a pre-existing house. In Canada, this is typically handled through a Construction Draw Mortgage (also known as a...

Read Post

April 22 2026

If you’re self-employed in Nova Scotia, refinancing your mortgage can feel a lot more complicated than it should be.

I’ve been a mortgage broker in Nova Scotia for over 22 years and co-own Mortgage Managers brokerage, and I can tell you this: being...

Read Post

April 20 2026

Read Post

April 14 2026

Surviving the 2026 Mortgage Renewal Wave: Your Survival Guide

The "Great Renewal Wave" isn't just a headline anymore—it’s officially landing on our doorsteps. If you were one of the thousands of Canadians who locked in a record-low mortgage rate back in 2021, you&rsquo...

Read Post

April 09 2026

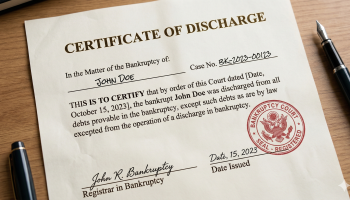

Yes, it is absolutely possible to get a mortgage after being discharged from bankruptcy. While it does require some strategic planning and patience, many Canadians successfully return to homeownership within a few years of their discharge.

The path you take generally depends on how long you are...

Read Post

April 08 2026

Saving for a down payment is often the biggest hurdle to homeownership. In Canada, the minimum down payment is 5% for homes under $500,000 and increases for more expensive properties. For homes between $500,000 and $1,500,000, the down payment is calculated on 5% of the first $500,000, then 10% on the amount above $500,000.

Read Post

April 07 2026

Check out the interest savings by going with a shorter Amortization. You can have the same impact on your mortgage by taking advantage of your Pre-payment Privledge of increasing your payment anually.

Read Post

April 06 2026

Buying your first home is one of the most exhilarating milestones you’ll ever reach. But in the 2026 real estate market—where inventory is shifting and lending criteria are stricter than ever—it’s also a high-stakes financial maneuver.

Even a small misstep...

Read Post

April 01 2026

In Canada, a high-ratio mortgage is any mortgage where your down payment is less than 20% of the home's purchase price.

Because you are putting down a smaller amount, the loan-to-value (LTV) ratio is "high" (over 80%). Under Canadian federal law, these mortgages must be protected by mortgage...

Read Post

March 30 2026

The monthly payment on a $400,000 mortgage depends on your interest rate and your amortization period (how long you take to pay it off). In the current March 2026 market, where rates have stabilized, you’re looking at a range of $1,900 to $2,350 per month.

Here is a breakdown...

Read Post

March 29 2026

In Canada, mortgage qualification is primarily determined by two debt-service ratios: the Gross Debt Service (GDS) and Total Debt Service (TDS) ratios. With an annual income of $70,000, your qualifying amount depends on your existing debts, your down payment, and current interest rates.

The Estimated Approval Range

...

Read Post

March 28 2026

The Interest Rate Differential (IRD) penalty is notorious for being expensive and confusing, primarily because major banks don’t just compare your current rate to today's rates—they use a "Posted Rate" calculation that often inflates the fee.

Here is the step-by-step breakdown of...

Read Post

March 28 2026

This remains the #1 question. In 2026, affordability is the primary hurdle for most borrowers.

The Answer: Lenders don't just look at what you can pay today; they test if you could still afford the mortgage payment if rates rose. The "Stress Test" makes borrowers qualify...

Read Post

March 27 2026

Will Canadian Mortgage Rates Go Down in 2026? What Experts Are Predicting

For years, Canadian homeowners and hopeful buyers have been riding a mortgage rate rollercoaster. From the ultra-low rates of the pandemic to a series of aggressive hikes, everyone is looking for signs of what's next....

Read Post

March 26 2026

For many Canadian homeowners reaching retirement in 2026, the term "house rich, cash poor" has never felt more accurate. With the Bank of Canada recently holding the policy rate at 2.25%, the real estate market in areas like Nova Scotia remains a massive source of untapped wealth.

A Canadian...

Read Post

March 26 2026

If you are one of the millions of entrepreneurs, freelancers, or small business owners driving the economy in 2026, you already know that "being your own boss" comes with incredible perks—and one major headache: getting a mortgage.

While your salaried friends simply hand over a T4...

Read Post