What do I need to know about getting a Construction Draw mortgage?

April 27 2026

Building your dream home in Nova Scotia from the ground up is an exhilarating journey, but from a financing perspective, it’s a bit of a different beast than buying a pre-existing house. In Canada, this is typically handled through a Construction Draw Mortgage (also known as a Progress Draw Mortgage).

As of 2026, new regulations and tax rebates have made this process even more nuanced. If you’re planning to break ground this year, here is everything you need to know to navigate the application and the build.

1. How a Draw Mortgage Actually Works

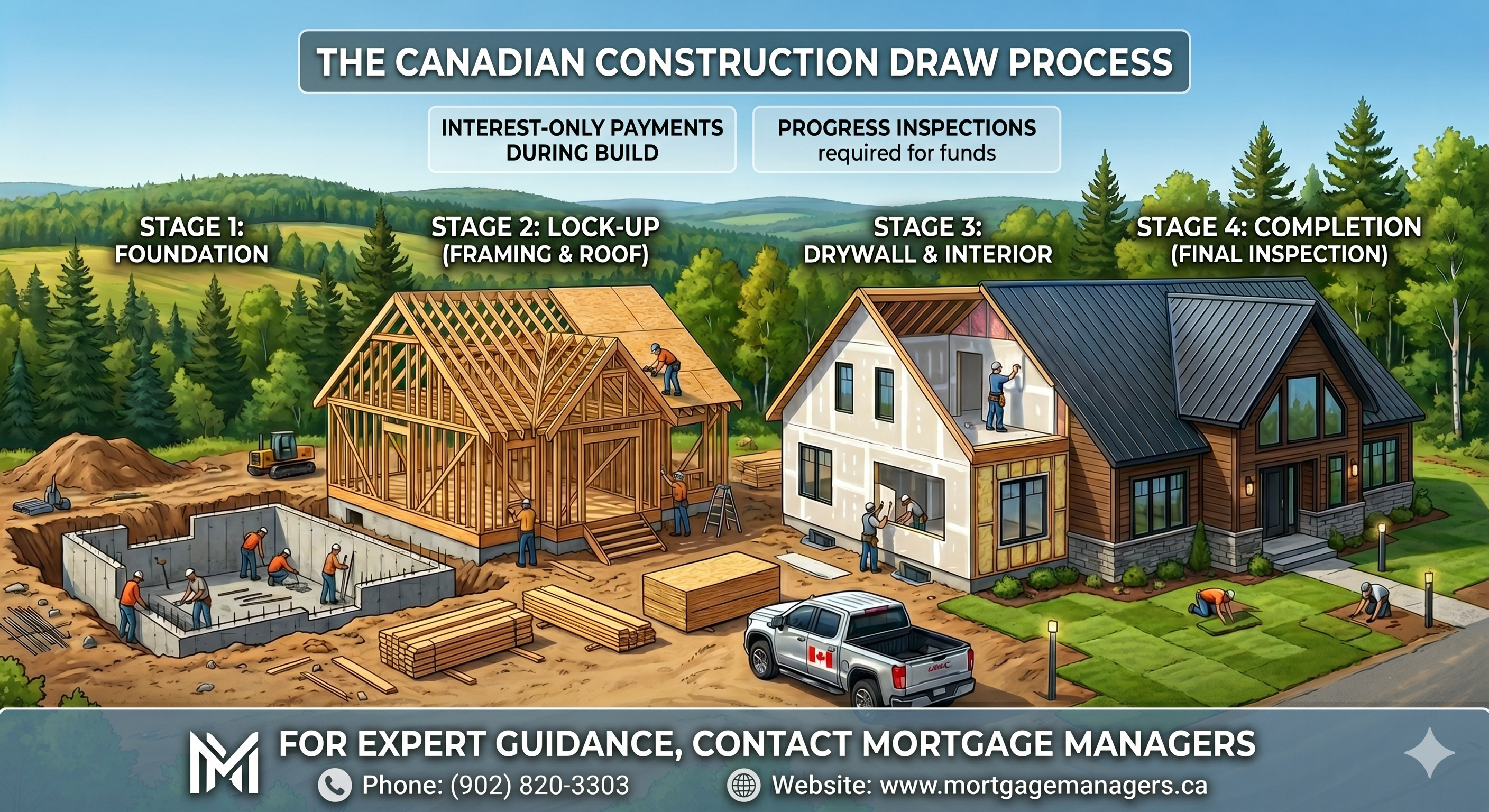

Unlike a traditional mortgage where the bank hands over a lump sum on closing day, a Draw Mortgage releases money in stages as your home is built.

Typically, lenders divide the build into four or five "draws" based on milestones:

- Foundation: The excavation is done and the concrete is poured.

- Lock-up: The roof is on, and windows/doors are installed (the house is weatherproof).

- Drywall: Interior walls are up and taped.

- Completion: The home is finished and ready for occupancy.

The Catch: You only pay interest on the money that has been "drawn" so far. If you've only used $100,000 of a $500,000 loan, your monthly payments will reflect only that $100k—usually as interest-only payments until construction is finished.

2. The Critical "10% Statutory Holdback"

This is the part that catches many Canadians off guard. Under provincial Construction Lien Acts, lenders are legally required to hold back 10% of every draw.

Why? This protects you (and the lender) from being liable if your main contractor fails to pay their sub-contractors or suppliers. If a plumber isn't paid, they can put a lien on your property. That 10% fund ensures there is cash available to settle those claims. You only release this money to the builder once the "lien period" (usually 45–60 days after completion) has expired.

3. 2026 Requirements & Documentation

Applying for a construction mortgage is paperwork-heavy. To get approved in 2026, you will need:

- Own the Land: The land must be in your name and be free & clear of any mortgages. The value of the land is your down payment.

- Building Permits & Plans: Lenders won't even look at your application without a municipal building permit and a full set of blueprints.

- A Detailed Budget: You need a line-by-line cost estimate. In 2026, many lenders now require a 10-15% contingency fund built into your budget to account for material price volatility.

- The Contract: Whether you are doing a "Contract Build" (hiring a pro) or a "Self-Build" (doing it yourself), the lender needs to see the signed agreement.

- Credit & Income: Expect the usual: a minimum credit score of 600 (though 680+ gets better rates), and debt-to-income ratios (GDS/TDS) capped at 39%/44%.

4. Draw vs. Completion Mortgages

Before you apply, make sure you’re choosing the right type of construction financing:

Progress Draw: Best for custom builds where the builder needs cash during the process to pay for materials and labor.

Completion Mortgage: Common in new subdivisions. You put a deposit down, and the builder finances the build themselves. You don't pay the full mortgage until the day you get the keys.

5. The 2026 "New Home" Financial Perks

The Canadian government and provinces have introduced significant incentives that apply to construction draws in 2026:

The Federal GST/HST Rebate

As of March 2026, the federal government offers a 100% GST rebate for first-time buyers on newly built homes priced up to $1,000,000, with a partial rebate for homes up to $1,500,000. If you are building your own home, you can claim this after the house is "substantially complete."

6. Pro-Tip: The Appraisal Trap

Lenders will send an appraiser to your site before each draw. If the appraiser decides the work is only 30% done but your builder says they’ve finished 45%, the bank will only pay for 30%.

The Strategy: Always keep a "bridge" of personal cash or a line of credit available. Construction almost always hits delays or budget gaps, and you don’t want your build to stall because of a 5% difference in an appraiser’s report.

Have you already selected a builder, or are you still in the planning phase?