Where can a Down Payment come from?

April 08 2026

Saving for a down payment is often the biggest hurdle to homeownership. In Canada, the minimum down payment is 5% for homes under $500,000 and increases for more expensive properties. For homes between $500,000 and $1,500,000, the down payment is calculated on 5% of the first $500,000, then 10% on the amount above $500,000.

Here are the top 10 most common sources used to fund a down payment:

1. Personal Savings & TFSAs

This is the most straightforward source. Funds held in chequing accounts, high-interest savings accounts (HISA), or a Tax-Free Savings Account (TFSA) are widely accepted. Lenders typically require 90 days of bank statements to verify the funds were not recently borrowed.

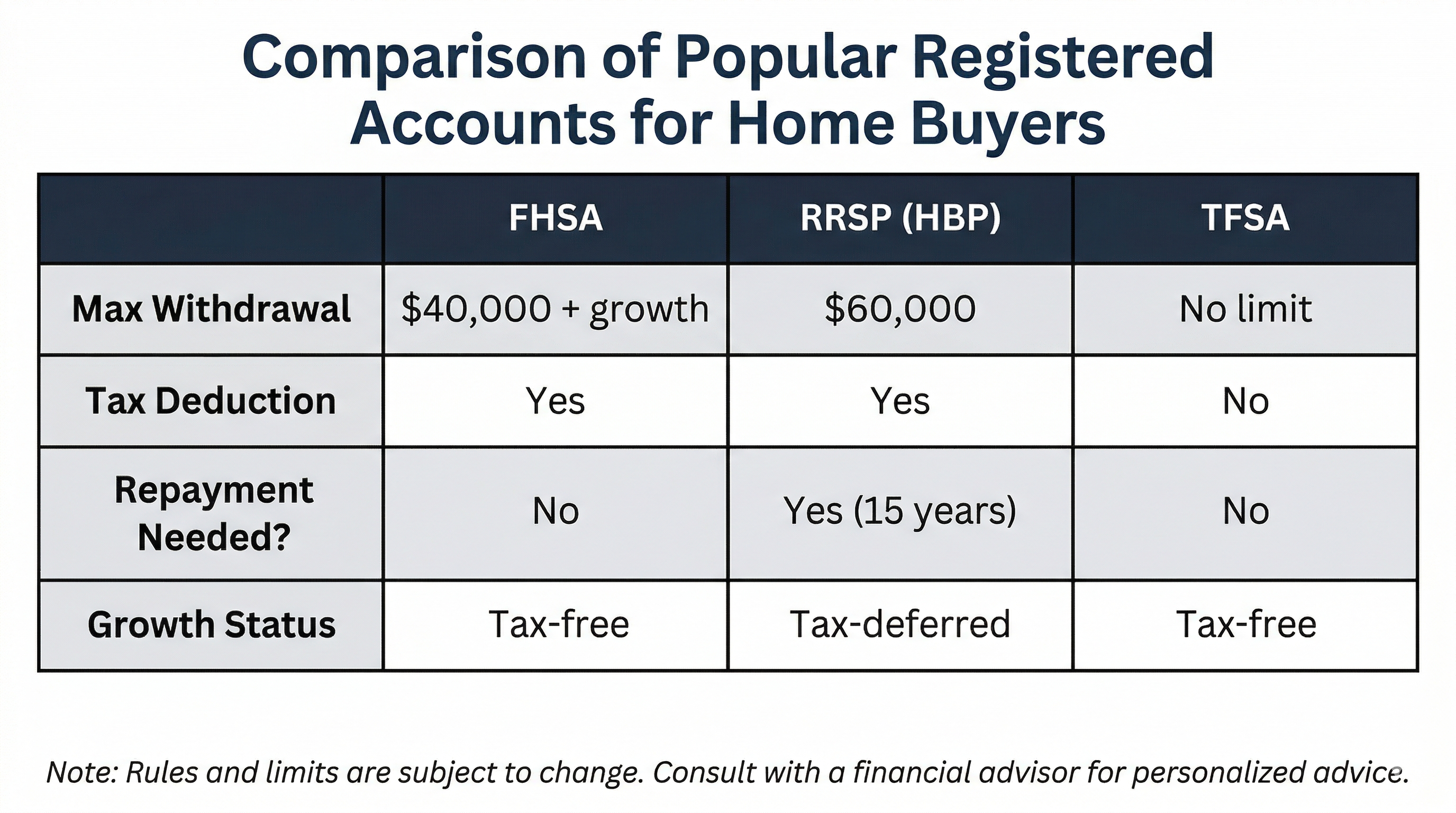

2. First Home Savings Account (FHSA)

A newer and highly popular tool, the FHSA allows you to contribute up to $8,000 per year (to a lifetime limit of $40,000). Like an RRSP, contributions are tax-deductible, but like a TFSA, withdrawals for a home purchase are completely tax-free and do not need to be repaid.

3. RRSP Home Buyers’ Plan (HBP)

First-time buyers can withdraw up to $60,000 from their Registered Retirement Savings Plan (RRSP) tax-free. You must repay the amount to your RRSP over a 15-year period, usually starting the second or fifth year after the withdrawal, depending on recent legislative changes.

4. Gifted Funds from Family

A non-repayable financial gift from an immediate family member (parents, siblings, or grandparents) is a very common source. To use this, you’ll need a signed Gift Letter stating the money is not a loan and does not need to be repaid.

5. Proceeds from the Sale of a Property

If you already own a home, the equity gained from its sale is a primary source for your next down payment. Lenders will ask for the Agreement of Purchase and Sale and a current mortgage statement to verify the net proceeds.

6. Investments (Stocks, Bonds, GICs)

Liquifying non-registered investments is a standard practice. Be mindful of potential capital gains taxes when selling stocks or the timing of GIC maturities to ensure the cash is available before your closing date.

7. Borrowed Funds (Lines of Credit/Loans)

While less common for "high-ratio" mortgages (less than 20% down), some lenders allow you to borrow your down payment via a Personal Line of Credit or loan. This is considered a "non-traditional" source and usually requires a higher credit score and potentially a higher insurance premium.

8. Sweat Equity

For those building their own home, "sweat equity" refers to the value of labor you contribute to the construction. CMHC and other insurers may allow this to account for a portion of the down payment, though it rarely covers the full 5% minimum.

9. Rent-to-Own Credits

In a rent-to-own agreement, a portion of your monthly rent is often set aside as a "rent credit." Over time, these credits accumulate to form your down payment when you eventually exercise your option to buy the home. There are strict rules around this. Consult a Mortgage Managers broker for details.

10. Government Assistance Programs

Federal and provincial programs can provide a boost. For example, in Nova Scotia, the Down Payment Assistance Program (DPAP) offers interest-free loans of up to 5% of the purchase price for eligible first-time buyers.